This page deals with prudential, conduct, outsourcing and AML Rules for emoney institutions and payments institutions. Click the download button for version 1.0 (31 October 2021).

Our Peter Oakes has written comprehensive guides on Why Ireland For Fintech for:

These guides have been downloaded 15,000+ times

If there is no link to a document you are looking for, contact office@complireg.com.

Please be respectful of the author's copyright and don't reproduce any part of this material for commercial purposes. If you leverage content from this page/document for your any other use, please acknowledge the author.

Other guides for a fintech authorisation can be found here.

Our Peter Oakes has written comprehensive guides on Why Ireland For Fintech for:

- securing an Electronic Money Authorisation;

- securing a Payment Institution Authorisation (which includes AISP and PISPs);

- securing a Virtual Asset Services Provider Registration;

- securing a MiFID authorisation;

- Overview of Certain Prudential, Conduct of Business Rules, Outsourcing and AML/CFT Guide.

These guides have been downloaded 15,000+ times

If there is no link to a document you are looking for, contact office@complireg.com.

Please be respectful of the author's copyright and don't reproduce any part of this material for commercial purposes. If you leverage content from this page/document for your any other use, please acknowledge the author.

Other guides for a fintech authorisation can be found here.

Why Ireland for Fintech? (Overview of Certain Prudential, Conduct of Business Rules, Outsourcing and AML/CFT Guide.) [V1.0 31 October 2021]

Congratulations. You have made a great decision: Ireland is fantastic place to obtain a payment institution authorisation (“API / payments institution”) from the Central Bank of Ireland (“CBI”). If you are seeking authorisation as an electronic money institution (“AEMI / emoney institution”) or MiFID firm or registration as a Virtual Asset Services Provider (“VASP”) visit https://fintechireland.com/fintech-authorisations.html for those and other authorisation and regulatory guides.

You have found the right people to assist you obtain a presence in Ireland. Peter Oakes is recognised by Chambers & Partners in its Fintech 2021 and 2020 edition as a Band 1 leading fintech expert. Peter is a past member of the selection panel of the Fintech 50 Panel.

Congratulations. You have made a great decision: Ireland is fantastic place to obtain a payment institution authorisation (“API / payments institution”) from the Central Bank of Ireland (“CBI”). If you are seeking authorisation as an electronic money institution (“AEMI / emoney institution”) or MiFID firm or registration as a Virtual Asset Services Provider (“VASP”) visit https://fintechireland.com/fintech-authorisations.html for those and other authorisation and regulatory guides.

You have found the right people to assist you obtain a presence in Ireland. Peter Oakes is recognised by Chambers & Partners in its Fintech 2021 and 2020 edition as a Band 1 leading fintech expert. Peter is a past member of the selection panel of the Fintech 50 Panel.

In our Guides on Why Ireland for Fintech for Payments Institutions and Electronic Money Institutions, which focus on how to obtain an authorisation from the Central Bank of Ireland (“CBI”), we pointed out that other topics for authorised payments institutions (“API”) and authorised electronic money institutions (“AEMI”) include:

The purpose of this document is to provide our clients and others with further information about the regulatory environment for APIs and AEMIs, particularly after they obtain authorisation. This document and our API Guide and AEMI Guide are available here https://fintechireland.com/fintech-authorisations.html

- prudential supervision requirement;

- passporting provisions;

- conduct of business rules; and

- data protection.

The purpose of this document is to provide our clients and others with further information about the regulatory environment for APIs and AEMIs, particularly after they obtain authorisation. This document and our API Guide and AEMI Guide are available here https://fintechireland.com/fintech-authorisations.html

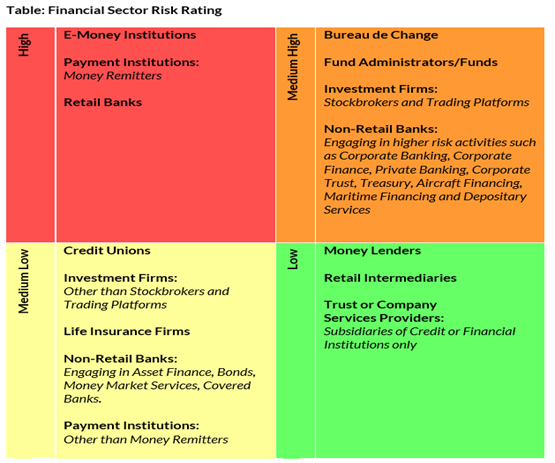

This CBI Risk Rating Document explained in our Overview Guide

Why Peter Oakes (www.peteroakes.com)

Peter Oakes is leading expert in fintech, including emoney, payments, crowdfunding, banking and investment management specialising in start-ups, governance, risk and compliance. Peter is a non-executive director of regulated emoney, payment services and investment services firms (investment advice and options market making). He is a former senior executive regulator in Australia (ASC/ASIC), the UK (FSA/FCA), Saudi Arabia (SAMA) and in Ireland (CBI). Between 2010-2013, Peter was appointed as Ireland’s inaugural director of enforcement and financial crime at the CBI. He was one of six individuals with an international background recruited into CBI at that time to address the economic and regulatory fallout arising from Ireland’s financial crisis.

During his time at the CBI he was involved in the implementation of numerous financial laws and regulations, including the regulations (PSD 1) preceding the European Communities (Payment Services) Regulations 2018 (the “PSR”) which transposed the Directive 2015/2336 (PSD 2) and including the European Communities (Electronic Money) Regulations 2011 (the “EMR”) which transposed the Directive 2009/110 into Ireland.

Since leaving the CBI in 2013, Peter has established the European payment services operations of Bank of America Merchant Services (including its authorisation as a PSD 2 firm with the UK FCA), led and supported numerous fintech authorisations with the UK FCA and the CBI. Peter worked on the application for a company which successfully achieved authorisation as a specialised bank with the Bank of Lithuania (“BoL”), including engagements with the BoL’s senior board director. Peter is a leading fintech and regulatory expert and the Founder of both Fintech Ireland[1] and Fintech UK[2]. Peter Oakes brings extensive practical experience and operational know-how to client instructions as well as unrivalled executive director, non-executive director and governance expertise, founded on a vast background of international regulator and central bank experience.

[1] https://fintechireland.com/index.html

[2] https://fintechuk.com/index.html

Peter Oakes is leading expert in fintech, including emoney, payments, crowdfunding, banking and investment management specialising in start-ups, governance, risk and compliance. Peter is a non-executive director of regulated emoney, payment services and investment services firms (investment advice and options market making). He is a former senior executive regulator in Australia (ASC/ASIC), the UK (FSA/FCA), Saudi Arabia (SAMA) and in Ireland (CBI). Between 2010-2013, Peter was appointed as Ireland’s inaugural director of enforcement and financial crime at the CBI. He was one of six individuals with an international background recruited into CBI at that time to address the economic and regulatory fallout arising from Ireland’s financial crisis.

During his time at the CBI he was involved in the implementation of numerous financial laws and regulations, including the regulations (PSD 1) preceding the European Communities (Payment Services) Regulations 2018 (the “PSR”) which transposed the Directive 2015/2336 (PSD 2) and including the European Communities (Electronic Money) Regulations 2011 (the “EMR”) which transposed the Directive 2009/110 into Ireland.

Since leaving the CBI in 2013, Peter has established the European payment services operations of Bank of America Merchant Services (including its authorisation as a PSD 2 firm with the UK FCA), led and supported numerous fintech authorisations with the UK FCA and the CBI. Peter worked on the application for a company which successfully achieved authorisation as a specialised bank with the Bank of Lithuania (“BoL”), including engagements with the BoL’s senior board director. Peter is a leading fintech and regulatory expert and the Founder of both Fintech Ireland[1] and Fintech UK[2]. Peter Oakes brings extensive practical experience and operational know-how to client instructions as well as unrivalled executive director, non-executive director and governance expertise, founded on a vast background of international regulator and central bank experience.

[1] https://fintechireland.com/index.html

[2] https://fintechuk.com/index.html

Next Steps?

Like what you have read? Contact Peter Oakes at peter@peteroakes.com (or office@complireg.com) to discuss how establishing an Authorised Payment Institution in Ireland is the wise choice and why Peter Oakes is the wise choice to assist.

Please also refer to our Overview of Certain Prudential and Conduct of Business Rules for Payment Institutions and Electronic Money Institutions available at https://fintechireland.com/fintech-authorisations.html for more detail about topics relevant to AEMIs / APIs.

Like what you have read? Contact Peter Oakes at peter@peteroakes.com (or office@complireg.com) to discuss how establishing an Authorised Payment Institution in Ireland is the wise choice and why Peter Oakes is the wise choice to assist.

Please also refer to our Overview of Certain Prudential and Conduct of Business Rules for Payment Institutions and Electronic Money Institutions available at https://fintechireland.com/fintech-authorisations.html for more detail about topics relevant to AEMIs / APIs.

This document is general guidance and information. It is not legal or other professional advice. Such advice should always be taken before acting on any of the matters discussed. If you need legal advice we can help with referral to a leading international law firm with operations in Dublin. This document draws upon information from Fintech Ireland, Fintech UK and CompliReg.

Version 1.0