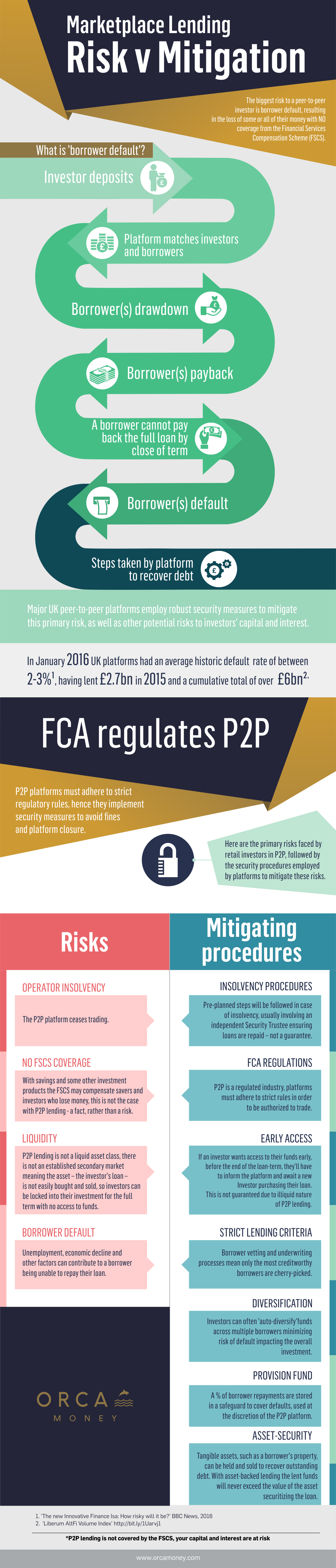

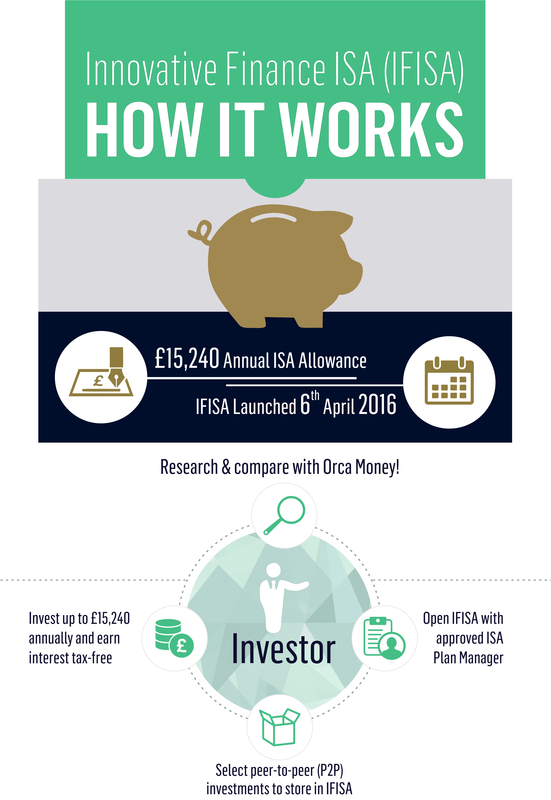

Thanks to Orca Money for sharing these useful graphics on Marketplace Lending (Risk v Mitigation) and Innovative Finance ISA. The graphics are below, however you might find the quality of these graphics better on Orca Money's website at:

- Orca Money's 'Risk v Mitigation' graphic available at https://www.orcamoney.com/p2p-lending-risk-mitigation

- Orca Money's 'Innovative Finance ISA' graphic available at https://www.orcamoney.com/ifisa-infographic