A copy of Peter Oakes' post on Linkedin

If you are:

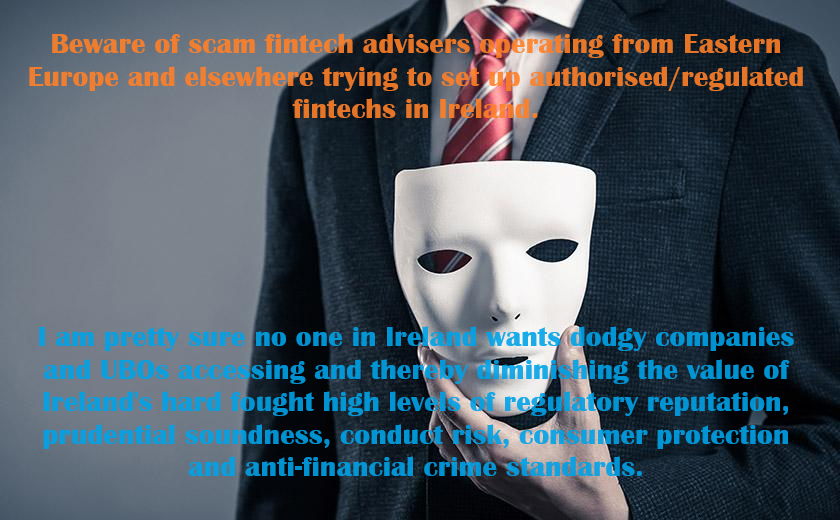

be very careful with what can only be described as middle-men sharks / charlatans operating in the industry claiming that they are based in Eastern Europe (inside and outside of the EU depending upon your questioning), that they have clients requiring authorisations in Ireland and that they need assistance from you with the business set-up and authorisation paperwork.

These sharks/charlatans mislead and lie about their credentials and their experience. It seems that Ireland has become the go to jurisdiction for firms wanting credible supervision and regulation and the sharks are trying to exploit this. However these middle-men/sharks have no idea of the regulatory regime in Europe, let alone Ireland, and a few pointed questions catch them out. Then the fun begins as you watch them squirm in their seats.

It is clear that these are the "fintech advisers" which have and continue to fail to get their clients authorised elsewhere (or are perhaps just a scam from the outset). With Ireland's reputation riding high, these sharks are bombarding me (and others) with poorly thought-out offers/plans. I think I receive at least four approaches a week from these bad actors.

Unusually, I took a call from one of these firms today. It was an advisory firm with a name I did not recognise. When the video feed went live it was the same person who approached me last year under a different corporate name. When he saw my face, the stuttering began. His lead generators had clearly let him down.

These firms try to hire/appoint people in Ireland and increase the amount of any fees guided upon and add a margin to 'their clients'. I asked if they disclose this margin to the underlying client? Together with that question, and a few other due diligence questions, they quickly got the message that Ireland doesn't welcome their type of business nor that of their clients.

I am pretty sure that no one in Ireland wants dodgy companies and UBOs accesses and thereby diminishing the value of Ireland's hard fought high levels of regulatory reputation, prudential soundness, conduct risk, consumer protection and anti-financial crime standards.

I am pretty sure that my peers in other EU Member States feel the same way.

- a regulatory adviser in Ireland, including a consultant, a law firm, an accounting firm,

- an aspiring CEO/CFO/CCO etc looking to join a fintech seeking authorisation,

- especially a founder looking to get his/her fintech (#emoney institution, #payments institution or #crypto asset institution),

- company formation firms (i.e. TCSPs), or

- a recruiter in the fintech arena,

be very careful with what can only be described as middle-men sharks / charlatans operating in the industry claiming that they are based in Eastern Europe (inside and outside of the EU depending upon your questioning), that they have clients requiring authorisations in Ireland and that they need assistance from you with the business set-up and authorisation paperwork.

These sharks/charlatans mislead and lie about their credentials and their experience. It seems that Ireland has become the go to jurisdiction for firms wanting credible supervision and regulation and the sharks are trying to exploit this. However these middle-men/sharks have no idea of the regulatory regime in Europe, let alone Ireland, and a few pointed questions catch them out. Then the fun begins as you watch them squirm in their seats.

It is clear that these are the "fintech advisers" which have and continue to fail to get their clients authorised elsewhere (or are perhaps just a scam from the outset). With Ireland's reputation riding high, these sharks are bombarding me (and others) with poorly thought-out offers/plans. I think I receive at least four approaches a week from these bad actors.

Unusually, I took a call from one of these firms today. It was an advisory firm with a name I did not recognise. When the video feed went live it was the same person who approached me last year under a different corporate name. When he saw my face, the stuttering began. His lead generators had clearly let him down.

These firms try to hire/appoint people in Ireland and increase the amount of any fees guided upon and add a margin to 'their clients'. I asked if they disclose this margin to the underlying client? Together with that question, and a few other due diligence questions, they quickly got the message that Ireland doesn't welcome their type of business nor that of their clients.

I am pretty sure that no one in Ireland wants dodgy companies and UBOs accesses and thereby diminishing the value of Ireland's hard fought high levels of regulatory reputation, prudential soundness, conduct risk, consumer protection and anti-financial crime standards.

I am pretty sure that my peers in other EU Member States feel the same way.