Fintech Ireland's Peter Oakes joined Petula Martyn on RTE's Morning Ireland Business Program to discuss competition in the payments market following news from the Competition and Consumer Protection Commission (CCPC) that it will carry out a Phase 2 investigation of proposed joint venture between AIB; BOI; PTSB and KBC to establish if the proposed transaction could lead to a substantial lessening of competition in the State. At the heart of the matter is a new industry-wide mobile payment system service, named Synch Payments DAC.

My LinkedIN post - https://www.linkedin.com/posts/peteroakes_fintech-payments-paytech-activity-6874672568347983872-Kki5

- AUDIO - LISTEN HERE

- Minutes of the Financial Stability Group 1 June 2021

- CCPC to carry out a Phase 2 investigation of proposed joint venture between AIB; BOI; PTSB and KBC

- Increasing competition in the digital payments market by Petula Martyn Thursday, 9 December 2021

My LinkedIN post - https://www.linkedin.com/posts/peteroakes_fintech-payments-paytech-activity-6874672568347983872-Kki5

On the radio this morning (for Fintech Ireland) on Ireland's national broadcaster RTE to discuss fintech and payments against the backdrop of the Competition and Consumer Protection Commission's announcement that it is moving to a Phase 2 competition investigation of the proposed joint venture between AIB; Bank of Ireland; permanent tsb and KBC Bank Ireland. At the heart of the matter is a new industry-wide mobile payment system service, named Synch Payments DAC.

The scope of the Phase 2 investigation is "in order to establish if the proposed transaction could lead to a substantial lessening of competition". Note the word 'could'. It is not 'will', 'might likely' or 'more likely than not will'. Thus no calling the race until the horse has crossed the line or not and all parties have been heard in a fair manner.

What was great about the discussion was ability to use real examples of fintech firms which are enabling customer (consumer and business) choice and fostering competition such as Anthony Watson's The Bank of London, Anne Boden's Starling Bank, Terry Clune's and Sinead Fitzmaurice's TransferMate Global Payments, bunq (which recently acquired another great fintech Capitalflow), N26 and Revolut.

One always over prepares for these discussions, but it does mean that you do a lot of useful research. For example:

If you get a chance, you should look at the minutes of the FSG 1 June meeting and the comments by the Central Bank. Its paper outlined a number of areas that related to the provision of banking services and merited deeper consideration, including:

The minutes also record that "Fintech entering the payment services market can have material implications for banks’ business models in the long-term", and that "Ireland also has a responsibility in our role as an EU/International banking sector, including for the digital infrastructure of that sector."

And while fintech and banks compete/collaborate, they'll need to continually keep an eye on #Web3 for payments! On that important topic, Read more at https://www.forbes.com/sites/forbestechcouncil/2020/01/06/what-is-web-3-0/?sh=59b4fe5258df

The scope of the Phase 2 investigation is "in order to establish if the proposed transaction could lead to a substantial lessening of competition". Note the word 'could'. It is not 'will', 'might likely' or 'more likely than not will'. Thus no calling the race until the horse has crossed the line or not and all parties have been heard in a fair manner.

- Interview here

- Minutes of the Financial Stability Group 1st June 2021

- CCPC announcement of Phase 2 investigation 8th December 2021

What was great about the discussion was ability to use real examples of fintech firms which are enabling customer (consumer and business) choice and fostering competition such as Anthony Watson's The Bank of London, Anne Boden's Starling Bank, Terry Clune's and Sinead Fitzmaurice's TransferMate Global Payments, bunq (which recently acquired another great fintech Capitalflow), N26 and Revolut.

One always over prepares for these discussions, but it does mean that you do a lot of useful research. For example:

- retail banks process circa 5 million transactions worth €3.7 billion every day (according to the Banking & Payments Federation Ireland).

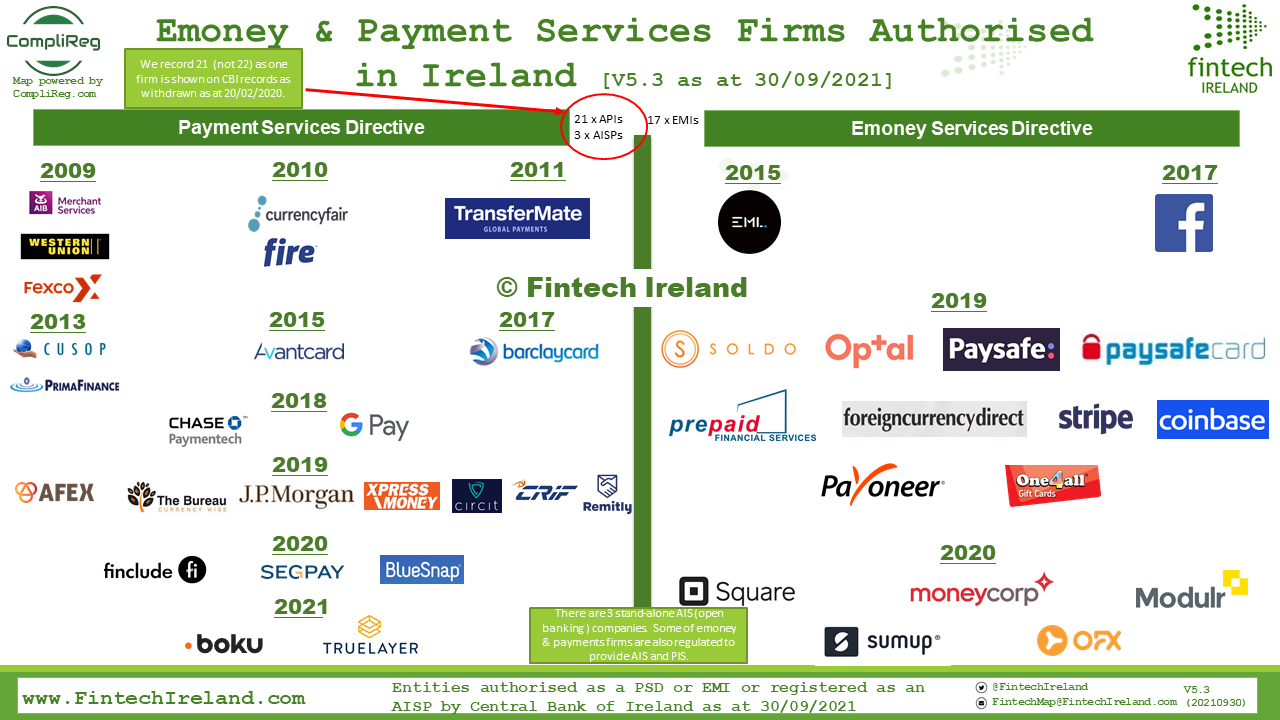

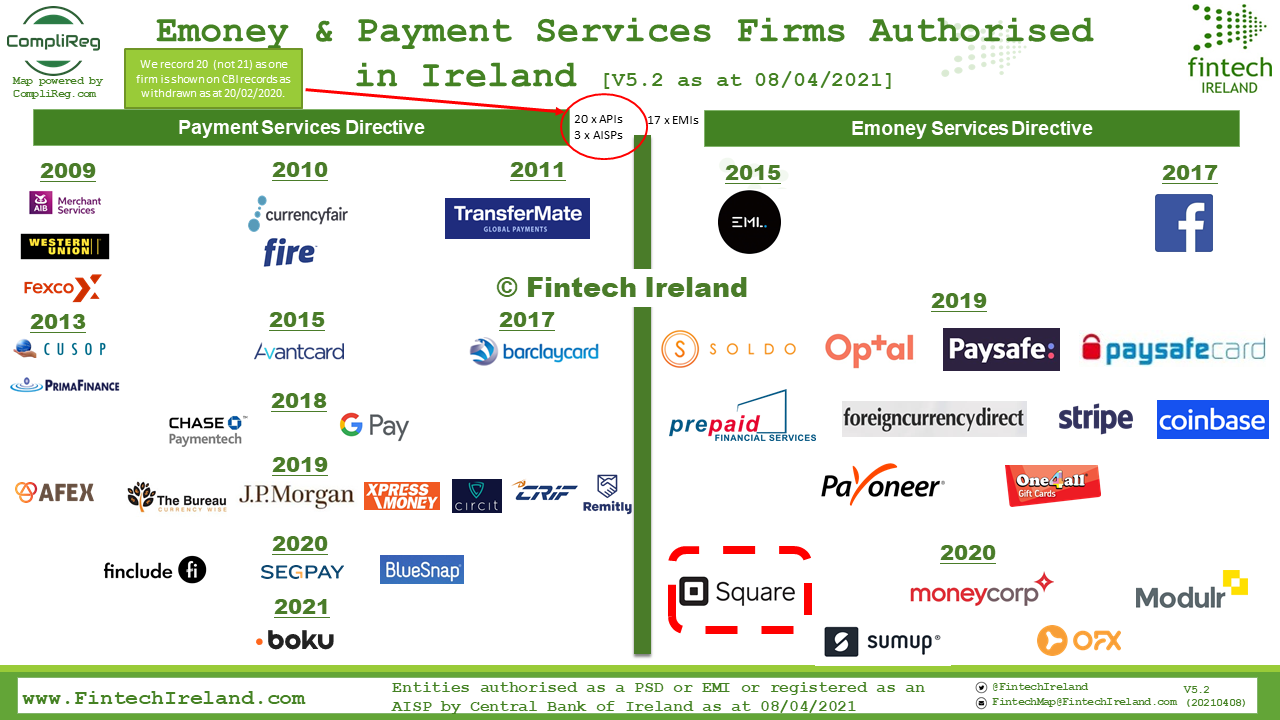

- there are more than 100 specialist #paytech firms operating in and from Ireland out of a wider pool of more than 385 fintech (see https://fintechireland.com/fintech-ireland-map.html)

- Ireland's Financial Stability Group discussed fintech competition for banks at its 1st June 2021 meeting. At that meeting the Central Bank of Ireland introduced a paper on the evolution of banking services in Ireland. The paper outlined the significant changes in the structure of the Irish financial system over the past decade and the factors that meant that – globally – the traditional banking business model has been under pressure. It also covered potential financial stability implications of the planned exit of two foreign-owned lenders from the Irish banking system.

If you get a chance, you should look at the minutes of the FSG 1 June meeting and the comments by the Central Bank. Its paper outlined a number of areas that related to the provision of banking services and merited deeper consideration, including:

- the trade-offs associated with actions that the banking system could take to generate capital in a sustainable way, as it adjusts to the evolving operating environment;

- the benefits and risks associated with the unbundling of traditional banking services and the growth in non-bank lenders;

- the main factors that might affect new entrants and/or the alternative provision of traditional banking services in Ireland.

The minutes also record that "Fintech entering the payment services market can have material implications for banks’ business models in the long-term", and that "Ireland also has a responsibility in our role as an EU/International banking sector, including for the digital infrastructure of that sector."

And while fintech and banks compete/collaborate, they'll need to continually keep an eye on #Web3 for payments! On that important topic, Read more at https://www.forbes.com/sites/forbestechcouncil/2020/01/06/what-is-web-3-0/?sh=59b4fe5258df