Welcome Zodia Markets to Fintech Ireland's Registered Virtual Asset Service Providers Map v 4

Fintech Ireland Newsletter: If you wish to receive the regular Fintech Ireland Newsletter for a round-up of fintech news and our events, sign-up here. We use MailChimp, so you can sign-up and unsubscribe with ease.

Since mid August 2023, it has been very quiet at the Virtual Asset Services Provider end of town when the then last VASP, MoonPay, was registered in Ireland on 15 August.

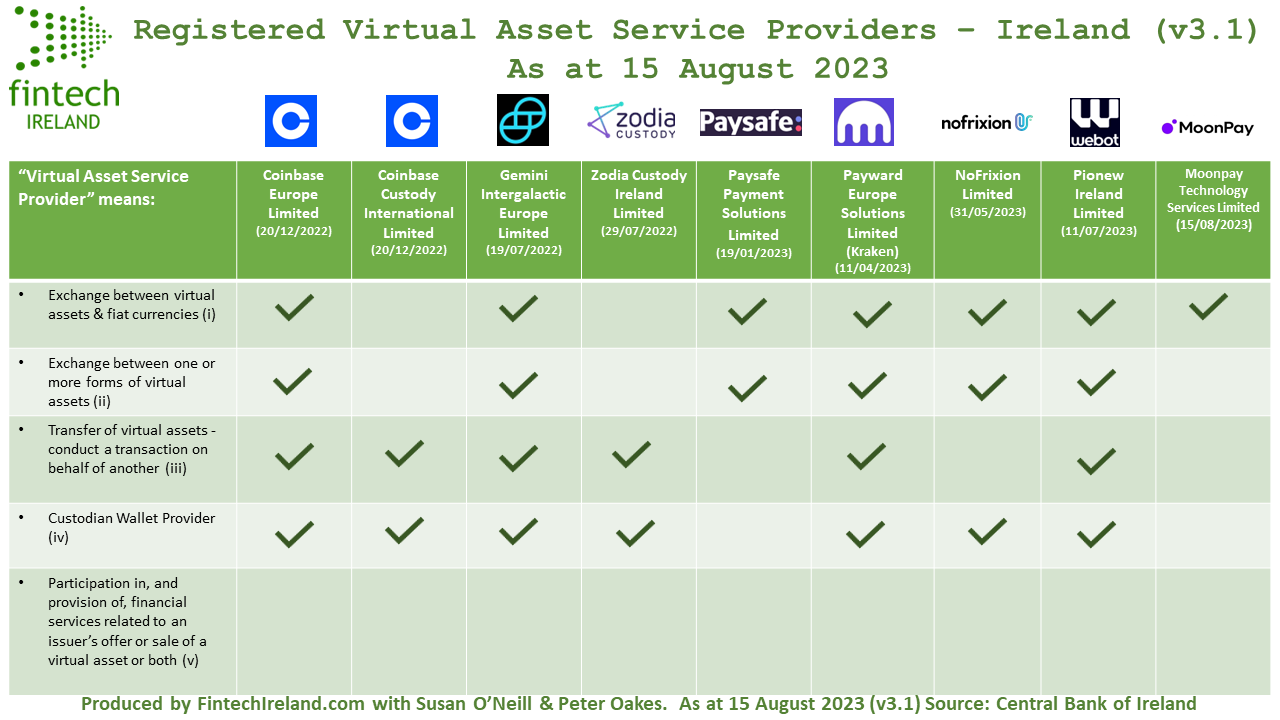

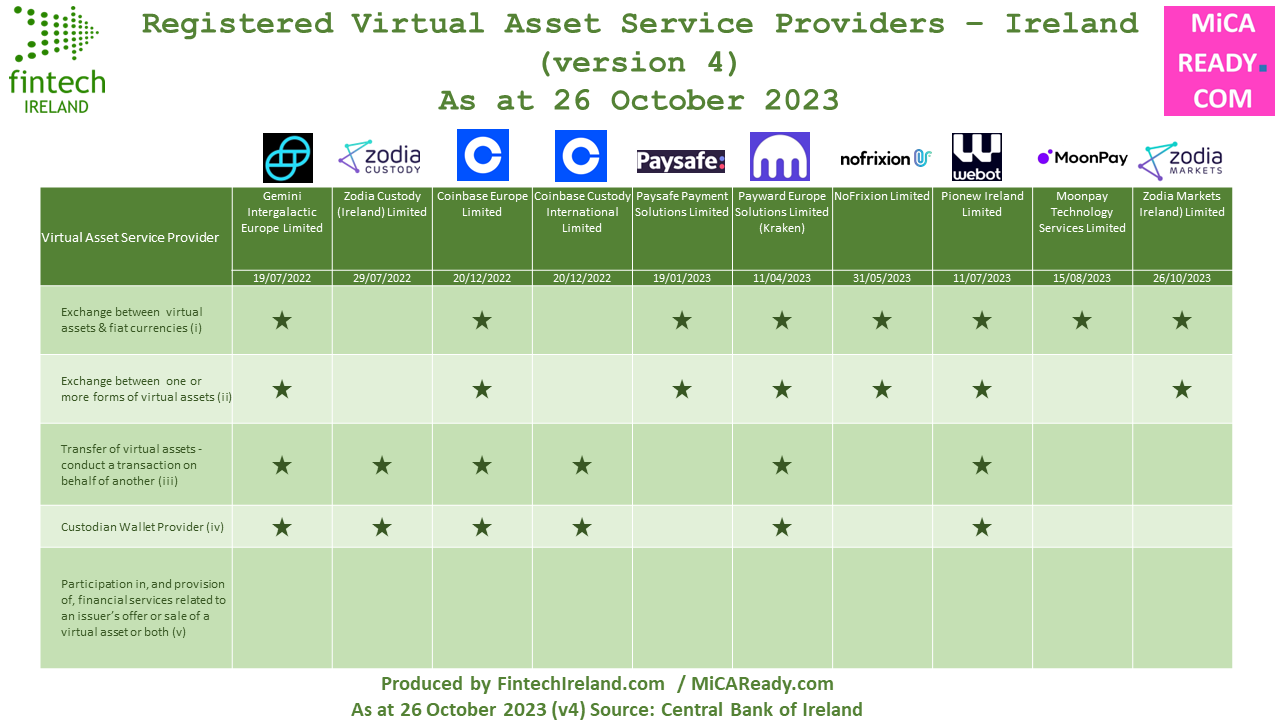

Fintech Ireland and MiCAReady.com have published version 4 of the Map (with assistance from Susan O’Neill of SuLu Solutions and Peter Oakes of Fintech Ireland), updated to include Zodia Markets (Ireland) Limited. Zodia Markets today (26 October 2023) joins Zodia Custody (Ireland) Limited, the latter which was registered back in July 2022, on version 4 of the Fintech Ireland Registered VASP Map.

The VASPs are registered by the Central Bank of Ireland for Anti Money Laundering/Countering the Financing of Terrorism purposes under Section 106A of the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021. They are not, as such, 'authorised' firms.

Welcome Zodia Markets (Ireland) Limited to the Map.

Zodia Markets was registered by the Central Bank of Ireland on 26 October 2023. Specifically, it is registered for service numbers: (i) exchange between virtual assets & fiat currencies; and (ii) the exchange between one or more forms of virtual assets. Zodia Custody is registered in Ireland for service numbers: (iii) transfer of virtual assets - conduct a transaction on behalf of another; and (iv) custodian wallet provider. Zodia Custody was the second of 10 VASP registered in Ireland when it became registered back on 29 June 2022.

Zodia Markets joins other registered virtual asset services firms including Coinbase Europe Limited, Coinbase Custody International Limited, Gemini Intergalactic Europe Limited, Zodia Custody Ireland Limited, Paysafe Payment Solutions Limited, NoFrixion Ireland Limited, Pionex Ireland Limited and MoonPay. Some of these crypto firms also hold an electronic money authorisation with the Central Bank of Ireland.

Zodia Market's local board of directors (according to Companies Registration Office records) are Nicholas Philpott and Michael Walsh. The VASP was incorporated on 16 June 2021.

In a statement released on Linkedin by Zodia Markets its Chief Executive Officer, Michael Walsh, commented: “The registration will act as a launchpad for the business to enter the EU, a market where we see significant opportunity and demand for our offering”. In the statement, Zodia Markets said "That this exciting development will enable it to provide services to clients throughout the European Union ahead of the implementation of the Markets of Cryptoassets Regulation.

BTW, Fintech Ireland and Peter Oakes are supporting both (1) MiCA Ready which tracks materially important EU news on MiCA and (2) Digital Assets Africa. If you need assistance with getting your VASP registered in Ireland or elsewhere in Europe reach out to Peter.

Don't forget to check out our Fintech Ireland Crypto Page.

Previous editions of the Map.

Fintech Ireland and MiCAReady.com have published version 4 of the Map (with assistance from Susan O’Neill of SuLu Solutions and Peter Oakes of Fintech Ireland), updated to include Zodia Markets (Ireland) Limited. Zodia Markets today (26 October 2023) joins Zodia Custody (Ireland) Limited, the latter which was registered back in July 2022, on version 4 of the Fintech Ireland Registered VASP Map.

The VASPs are registered by the Central Bank of Ireland for Anti Money Laundering/Countering the Financing of Terrorism purposes under Section 106A of the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021. They are not, as such, 'authorised' firms.

Welcome Zodia Markets (Ireland) Limited to the Map.

Zodia Markets was registered by the Central Bank of Ireland on 26 October 2023. Specifically, it is registered for service numbers: (i) exchange between virtual assets & fiat currencies; and (ii) the exchange between one or more forms of virtual assets. Zodia Custody is registered in Ireland for service numbers: (iii) transfer of virtual assets - conduct a transaction on behalf of another; and (iv) custodian wallet provider. Zodia Custody was the second of 10 VASP registered in Ireland when it became registered back on 29 June 2022.

Zodia Markets joins other registered virtual asset services firms including Coinbase Europe Limited, Coinbase Custody International Limited, Gemini Intergalactic Europe Limited, Zodia Custody Ireland Limited, Paysafe Payment Solutions Limited, NoFrixion Ireland Limited, Pionex Ireland Limited and MoonPay. Some of these crypto firms also hold an electronic money authorisation with the Central Bank of Ireland.

Zodia Market's local board of directors (according to Companies Registration Office records) are Nicholas Philpott and Michael Walsh. The VASP was incorporated on 16 June 2021.

In a statement released on Linkedin by Zodia Markets its Chief Executive Officer, Michael Walsh, commented: “The registration will act as a launchpad for the business to enter the EU, a market where we see significant opportunity and demand for our offering”. In the statement, Zodia Markets said "That this exciting development will enable it to provide services to clients throughout the European Union ahead of the implementation of the Markets of Cryptoassets Regulation.

BTW, Fintech Ireland and Peter Oakes are supporting both (1) MiCA Ready which tracks materially important EU news on MiCA and (2) Digital Assets Africa. If you need assistance with getting your VASP registered in Ireland or elsewhere in Europe reach out to Peter.

Don't forget to check out our Fintech Ireland Crypto Page.

Previous editions of the Map.