The balancing act of fintech: Inside Peter Oakes' quest for technological harmony

Imagine a world where your bank is as smart as your phone—but who keeps the tech in check? Enter the realm of Peter Oakes, fintech ecosystem builder and regtech expert. With over three decades of experience in the fintech, regulatory, and compliance sectors, Peter's journey is a tapestry of innovation and leadership.

Peter's career took flight at the Australian Securities & Investments Commission, where his early roles in enforcement set the stage for a lifetime dedicated to navigating the complex intersection of finance, technology, and regulation. His transition to the private sector in 2000 marked a new chapter, showcasing his versatility as he took up significant roles at Delaware Investments, Baring Asset Management, and BISYS Ireland, among others.

In 2010, Peter emerged as a pivotal figure during Ireland's financial crisis as the Director of Enforcement and Financial Crime at the Central Bank of Ireland. His efforts were instrumental in restoring trust in financial institutions during a tumultuous period.

Post-2013, Peter's focus shifted towards fintech, leading him to found Fintech Ireland and Fintech UK. These initiatives demonstrate his commitment to fostering fintech ecosystems in both countries. His venture CompliReg specializes in regulatory licensing and compliance for fintech companies.

Peter's career took flight at the Australian Securities & Investments Commission, where his early roles in enforcement set the stage for a lifetime dedicated to navigating the complex intersection of finance, technology, and regulation. His transition to the private sector in 2000 marked a new chapter, showcasing his versatility as he took up significant roles at Delaware Investments, Baring Asset Management, and BISYS Ireland, among others.

In 2010, Peter emerged as a pivotal figure during Ireland's financial crisis as the Director of Enforcement and Financial Crime at the Central Bank of Ireland. His efforts were instrumental in restoring trust in financial institutions during a tumultuous period.

Post-2013, Peter's focus shifted towards fintech, leading him to found Fintech Ireland and Fintech UK. These initiatives demonstrate his commitment to fostering fintech ecosystems in both countries. His venture CompliReg specializes in regulatory licensing and compliance for fintech companies.

Fintech Ecosystem Building

In our exclusive interview, Peter shared insights into what drove him to start Fintech Ireland and Fintech UK. "It was the time I was spending traveling between Ireland and the UK, setting up Bank of America's payment operations in London," he said. Peter recognized a disparity between the fintech industries in the two countries and was inspired to bridge that gap.

Peter observed that while Ireland had a fintech industry, it lacked the scale and complexity of the UK's. He collaborated with like-minded individuals like Dave Anderson and Peter O'Halloran to create a united front under the Fintech Ireland banner. "It was about creating a focal point, a unified domain to promote the Irish fintech ecosystem," he explained.

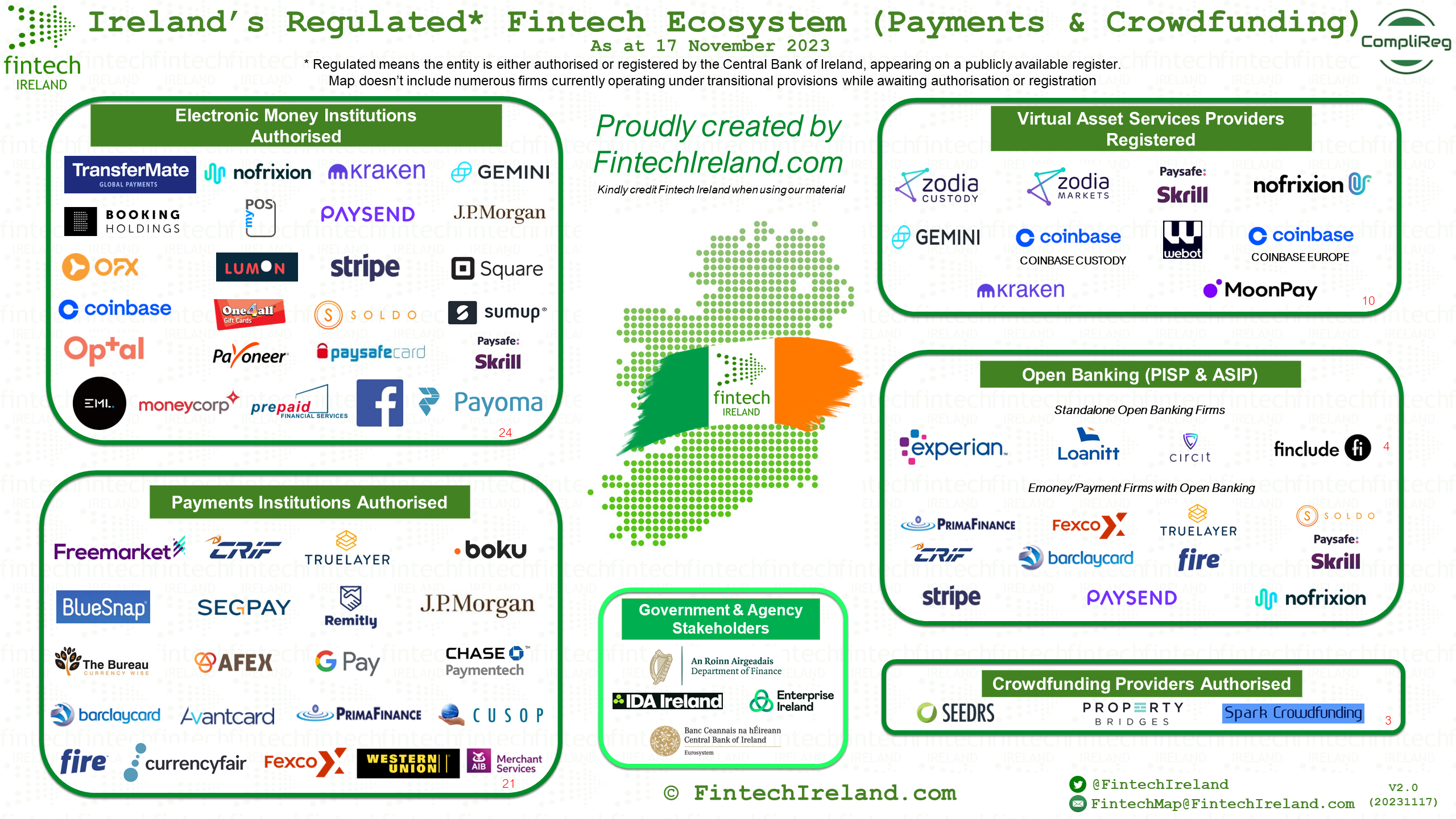

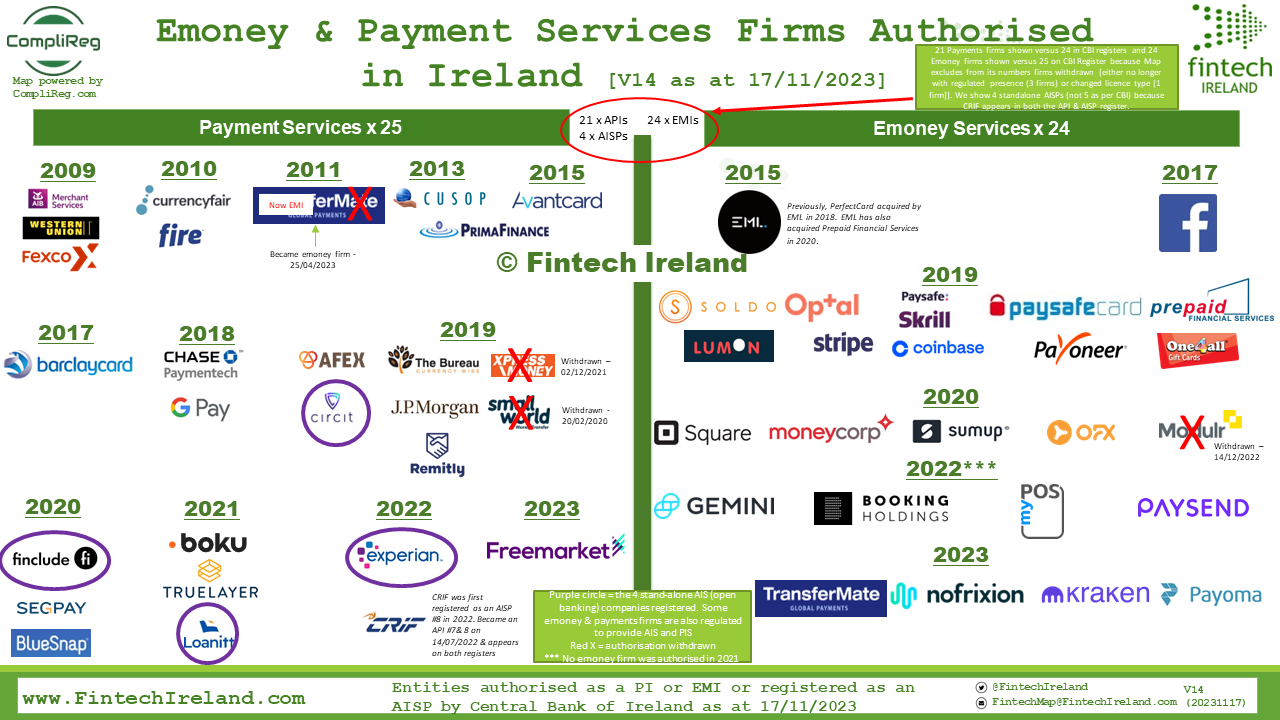

The impact of these initiatives has been significant. In 2013, Ireland had a handful of regulated fintech firms. Today, that number has grown exponentially. "We're now close to 50 regulated fintech firms in Ireland," Peter noted, highlighting the sector's growth in payment services, money, and open banking.

Peter's vision extends beyond just numbers. He has been instrumental in mapping the fintech landscape in Ireland, creating resources that list indigenous and international fintech firms operating in the country. "We're going to release updated maps soon, reflecting the dynamic changes in the ecosystem," he added.

Peter reflected on the origins of Fintech Ireland and Fintech UK, initiatives that stemmed from his keen observation of the fintech landscapes in both countries. "The UK is Ireland's largest trading partner," he noted, highlighting the critical trade relationship that spurred his efforts. His multinational background, having lived across continents since 1997, gives him a unique perspective on the global fintech scene.

Peter's foresight about Brexit's implications for trade and finance was a key motivator. "We knew Brexit would bring changes, and we wanted to ensure strong fintech ties between Ireland and the UK," he explained. This vision led to the creation of Fintech UK, aimed at bolstering interest in the Irish fintech sector and aiding Irish companies in navigating the UK's fintech landscape.

What sets Peter apart is his collaborative approach. "We've tried to be a strong voice, but not the only voice," he said, acknowledging the collective efforts of various stakeholders in shaping the Irish fintech ecosystem. This ecosystem has now embraced a multifaceted approach, with strategies focusing on finance, payments, and even artificial intelligence.

In our exclusive interview, Peter shared insights into what drove him to start Fintech Ireland and Fintech UK. "It was the time I was spending traveling between Ireland and the UK, setting up Bank of America's payment operations in London," he said. Peter recognized a disparity between the fintech industries in the two countries and was inspired to bridge that gap.

Peter observed that while Ireland had a fintech industry, it lacked the scale and complexity of the UK's. He collaborated with like-minded individuals like Dave Anderson and Peter O'Halloran to create a united front under the Fintech Ireland banner. "It was about creating a focal point, a unified domain to promote the Irish fintech ecosystem," he explained.

The impact of these initiatives has been significant. In 2013, Ireland had a handful of regulated fintech firms. Today, that number has grown exponentially. "We're now close to 50 regulated fintech firms in Ireland," Peter noted, highlighting the sector's growth in payment services, money, and open banking.

Peter's vision extends beyond just numbers. He has been instrumental in mapping the fintech landscape in Ireland, creating resources that list indigenous and international fintech firms operating in the country. "We're going to release updated maps soon, reflecting the dynamic changes in the ecosystem," he added.

Peter reflected on the origins of Fintech Ireland and Fintech UK, initiatives that stemmed from his keen observation of the fintech landscapes in both countries. "The UK is Ireland's largest trading partner," he noted, highlighting the critical trade relationship that spurred his efforts. His multinational background, having lived across continents since 1997, gives him a unique perspective on the global fintech scene.

Peter's foresight about Brexit's implications for trade and finance was a key motivator. "We knew Brexit would bring changes, and we wanted to ensure strong fintech ties between Ireland and the UK," he explained. This vision led to the creation of Fintech UK, aimed at bolstering interest in the Irish fintech sector and aiding Irish companies in navigating the UK's fintech landscape.

What sets Peter apart is his collaborative approach. "We've tried to be a strong voice, but not the only voice," he said, acknowledging the collective efforts of various stakeholders in shaping the Irish fintech ecosystem. This ecosystem has now embraced a multifaceted approach, with strategies focusing on finance, payments, and even artificial intelligence.

Entering the World of Fintech

Peter's engagement with fintech was not a sudden pivot but a gradual inclination fueled by his extensive experience in regulation and finance. His journey through the realms of regulatory technology and fintech began in the late 90s. He recalled, "I noticed that many issues in finance weren't just human errors but were often caused by poor technology deployment."

This realization led Peter to pioneer the use of regulatory technology tools in investment management, focusing on ensuring compliance with investment guidelines. "It was about building technology platforms that aligned with our clients' investment mandates," he shared, illustrating the intersection of technology and regulatory compliance.

Peter's consultancy work further deepened his involvement in fintech. He became a pivotal figure in authorizing the first fintech in Ireland and played a crucial role in shaping the industry's regulatory landscape. "We were at the forefront, learning new guidelines, and shaping the industry," Peter reflected on these formative experiences.

His time in London, working with Bank of America and other financial institutions, added layers to his expertise. Peter's role in setting up fintech firms, like Revolut, and his advisory positions in various fintech companies, have solidified his reputation as a visionary leader in the space.

Peter acknowledges the roots of fintech, noting early pioneers like First Direct in the UK and First-e in Ireland. His journey saw the fintech landscape evolve from its nascent stages to a dynamic, ever-changing field. He pointed out a notable shift in the industry: the rise of young, entrepreneurial talent. "There's a much more entrepreneurial spirit in society," Peter observed, attributing part of this shift to technological advancements and the changing landscape of work post-COVID.

He touched on the challenges that fintech entrepreneurs face, particularly in Europe, where failure is often seen less favorably than in the US. "There's a level of perseverance that entrepreneurs had," he said, highlighting the risks many took leaving comfortable jobs in traditional financial services for the uncertain world of fintech startups.

Peter's engagement with fintech was not a sudden pivot but a gradual inclination fueled by his extensive experience in regulation and finance. His journey through the realms of regulatory technology and fintech began in the late 90s. He recalled, "I noticed that many issues in finance weren't just human errors but were often caused by poor technology deployment."

This realization led Peter to pioneer the use of regulatory technology tools in investment management, focusing on ensuring compliance with investment guidelines. "It was about building technology platforms that aligned with our clients' investment mandates," he shared, illustrating the intersection of technology and regulatory compliance.

Peter's consultancy work further deepened his involvement in fintech. He became a pivotal figure in authorizing the first fintech in Ireland and played a crucial role in shaping the industry's regulatory landscape. "We were at the forefront, learning new guidelines, and shaping the industry," Peter reflected on these formative experiences.

His time in London, working with Bank of America and other financial institutions, added layers to his expertise. Peter's role in setting up fintech firms, like Revolut, and his advisory positions in various fintech companies, have solidified his reputation as a visionary leader in the space.

Peter acknowledges the roots of fintech, noting early pioneers like First Direct in the UK and First-e in Ireland. His journey saw the fintech landscape evolve from its nascent stages to a dynamic, ever-changing field. He pointed out a notable shift in the industry: the rise of young, entrepreneurial talent. "There's a much more entrepreneurial spirit in society," Peter observed, attributing part of this shift to technological advancements and the changing landscape of work post-COVID.

He touched on the challenges that fintech entrepreneurs face, particularly in Europe, where failure is often seen less favorably than in the US. "There's a level of perseverance that entrepreneurs had," he said, highlighting the risks many took leaving comfortable jobs in traditional financial services for the uncertain world of fintech startups.

Regulation: Tending a Garden of Tech

Reflecting on the broader implications of fintech, Peter noted how regulation can be both an enabler and an inhibitor. The balance between encouraging innovation and maintaining stability and trust in the financial system is delicate. This complexity was something he experienced first-hand during his tenure as the Director of Enforcement at the Central Bank of Ireland during the financial crisis.

Peter emphasized the critical role of trust in the financial system. The Irish financial crisis taught him the importance of rebuilding trust, not just in the banks but also in the regulatory framework itself. "Trust is the word that just keeps coming up," he reiterated. The crisis necessitated a restructure of the Central Bank and the implementation of a more robust regulatory framework, under the watchful eye of the EU.

The lessons from this period were profound. Peter and his team had to navigate a fine line between enforcing new regulations and being empathetic towards sectors that were not responsible for the crisis. This experience highlighted the importance of balanced regulation – ensuring financial stability and market integrity while protecting consumer interests.

As for the future of fintech, Peter sees a landscape ripe with innovation, moving towards concepts like decentralized finance and digital autonomous organizations. "We're moving into a much more interesting world of Web 3.0," he remarked, hinting at the untapped potential of this new digital era.

Peter discusses regulation in the fintech and AI spaces using an extremely compelling analogy. "Think about regulation like the hose at the back of the house," he said. "Sometimes you need a full flow, other times a gentle spray." This metaphor illustrates the nuanced approach needed in regulation — not a one-size-fits-all solution but a calibrated response tailored to specific needs and situations.

When it comes to fintech, Peter pointed out the importance of not stifling innovation. Over-regulation, especially of young fintech companies, could strangle both the business and the market it serves. He argues for a balanced approach, ensuring businesses are run by fit and proper individuals who make wise decisions. "Regulation should focus on the outcomes and the systems and controls in place, rather than the technology itself," Peter explained.

Peter's perspective on blockchain technology also challenges conventional thinking. He provocatively asked, "Isn't blockchain essentially an Excel spreadsheet across thousands of Dropboxes?" This analogy underscores his view that not all technologies necessitate specific regulatory frameworks. Instead, the focus should be on how these technologies are implemented within financial services.

Looking ahead, Peter anticipates more discussions and potential regulations around AI in the financial sector. However, he maintains that a cautious approach is necessary. "We need to think carefully about regulating AI in financial services, as the path we choose could have far-reaching implications," he cautioned.

Reflecting on the broader implications of fintech, Peter noted how regulation can be both an enabler and an inhibitor. The balance between encouraging innovation and maintaining stability and trust in the financial system is delicate. This complexity was something he experienced first-hand during his tenure as the Director of Enforcement at the Central Bank of Ireland during the financial crisis.

Peter emphasized the critical role of trust in the financial system. The Irish financial crisis taught him the importance of rebuilding trust, not just in the banks but also in the regulatory framework itself. "Trust is the word that just keeps coming up," he reiterated. The crisis necessitated a restructure of the Central Bank and the implementation of a more robust regulatory framework, under the watchful eye of the EU.

The lessons from this period were profound. Peter and his team had to navigate a fine line between enforcing new regulations and being empathetic towards sectors that were not responsible for the crisis. This experience highlighted the importance of balanced regulation – ensuring financial stability and market integrity while protecting consumer interests.

As for the future of fintech, Peter sees a landscape ripe with innovation, moving towards concepts like decentralized finance and digital autonomous organizations. "We're moving into a much more interesting world of Web 3.0," he remarked, hinting at the untapped potential of this new digital era.

Peter discusses regulation in the fintech and AI spaces using an extremely compelling analogy. "Think about regulation like the hose at the back of the house," he said. "Sometimes you need a full flow, other times a gentle spray." This metaphor illustrates the nuanced approach needed in regulation — not a one-size-fits-all solution but a calibrated response tailored to specific needs and situations.

When it comes to fintech, Peter pointed out the importance of not stifling innovation. Over-regulation, especially of young fintech companies, could strangle both the business and the market it serves. He argues for a balanced approach, ensuring businesses are run by fit and proper individuals who make wise decisions. "Regulation should focus on the outcomes and the systems and controls in place, rather than the technology itself," Peter explained.

Peter's perspective on blockchain technology also challenges conventional thinking. He provocatively asked, "Isn't blockchain essentially an Excel spreadsheet across thousands of Dropboxes?" This analogy underscores his view that not all technologies necessitate specific regulatory frameworks. Instead, the focus should be on how these technologies are implemented within financial services.

Looking ahead, Peter anticipates more discussions and potential regulations around AI in the financial sector. However, he maintains that a cautious approach is necessary. "We need to think carefully about regulating AI in financial services, as the path we choose could have far-reaching implications," he cautioned.

Envisioning the Future

Peter's nuanced understanding of the complex interplay between technology and regulation in the financial world is not just a story of adaptation and foresight; it is a roadmap for navigating the uncharted territories of fintech and AI. His analogy of regulation as a garden hose – requiring careful adjustment according to the needs of the moment – captures the essence of his approach: adaptable, measured, and always mindful of the delicate ecosystems it aims to nurture.

One of the most thought-provoking takeaways from Peter's insights is the potential for a paradigm shift in how we view and regulate emerging technologies. His questioning of whether technologies like blockchain should be regulated in the same manner as traditional financial services challenges current regulatory frameworks.

As we look to the future, one can't help but wonder about the next frontier in fintech and regulation. Peter's journey suggests a future where regulation harmonizes with innovation, where new technologies are not just integrated into existing frameworks but inspire new ways of thinking about finance and regulation. In this future, the fintech landscape is not just a field of competition but a collaborative ecosystem where innovation thrives.

Stay turned for Part 2 of our discussion with Peter Oakes – including the full video interview.

Peter's nuanced understanding of the complex interplay between technology and regulation in the financial world is not just a story of adaptation and foresight; it is a roadmap for navigating the uncharted territories of fintech and AI. His analogy of regulation as a garden hose – requiring careful adjustment according to the needs of the moment – captures the essence of his approach: adaptable, measured, and always mindful of the delicate ecosystems it aims to nurture.

One of the most thought-provoking takeaways from Peter's insights is the potential for a paradigm shift in how we view and regulate emerging technologies. His questioning of whether technologies like blockchain should be regulated in the same manner as traditional financial services challenges current regulatory frameworks.

As we look to the future, one can't help but wonder about the next frontier in fintech and regulation. Peter's journey suggests a future where regulation harmonizes with innovation, where new technologies are not just integrated into existing frameworks but inspire new ways of thinking about finance and regulation. In this future, the fintech landscape is not just a field of competition but a collaborative ecosystem where innovation thrives.

Stay turned for Part 2 of our discussion with Peter Oakes – including the full video interview.