Authors picture London taxi 2022

This article is written by Fintech Ireland Advisory Council Member and payments expert Rónán Gallagher. More about Rónán at the end of his article.

To stay abreast of developments at FintechHub.ie sign up to our Newsletter HERE

While undoubtedly Covid-19 encouraged an increase in electronic payments in Ireland and most other countries it seems we may not quite be ready for a cashless society just yet as increasingly there are conversations around access to and acceptance of cash.

In December 2023 Minister for Finance, Michael McGrath TD launched a public consultation on a National Payment Strategy for Ireland. At the consultation launch at the Banking & Payments Federation Ireland BPFI, parts of his speech gave an insight into the government’s view on the place of cash within a future payments strategy: “All citizens should be able to participate fully in all aspects of modern life using digital or cash methods of payment. .. I want to ensure choice is at the centre of our future payments strategy. We must recognise the important role that cash continues to play in our society and economy, and this is a role I am determined to protect.”

In the week following the consultation launch RTÉ reported that Minister McGrath called on the National Driving Licence Service to reinstate cash acceptance for driving licences at their centres around the country: "I expect all essential public services provided by the State and on behalf of the State to be accessible to members of the public whose preference is to transact in cash." His statement echoed previous government sentiment on cash acceptance which included the Minister writing to his government colleagues in September requesting that public bodies under their control maintain existing cash payment facilities pending the outcome of the National Payments Strategy.

In December 2023 Minister for Finance, Michael McGrath TD launched a public consultation on a National Payment Strategy for Ireland. At the consultation launch at the Banking & Payments Federation Ireland BPFI, parts of his speech gave an insight into the government’s view on the place of cash within a future payments strategy: “All citizens should be able to participate fully in all aspects of modern life using digital or cash methods of payment. .. I want to ensure choice is at the centre of our future payments strategy. We must recognise the important role that cash continues to play in our society and economy, and this is a role I am determined to protect.”

In the week following the consultation launch RTÉ reported that Minister McGrath called on the National Driving Licence Service to reinstate cash acceptance for driving licences at their centres around the country: "I expect all essential public services provided by the State and on behalf of the State to be accessible to members of the public whose preference is to transact in cash." His statement echoed previous government sentiment on cash acceptance which included the Minister writing to his government colleagues in September requesting that public bodies under their control maintain existing cash payment facilities pending the outcome of the National Payments Strategy.

During 2023 many organisations were criticised for their stance on cash acceptance. The National Ploughing Championship organise one of the largest spectator events in Ireland with over 200,000 attending in 2023. They introduced an online pre-purchase for the event to manage visitor numbers and this decision to not accept cash at the gates was described as an affront to the people of Ireland by one TD (Teachta Dála – a member of the Dáil, the lower house of the Irish Parliament). The Gaelic Athletic Association (GAA) have also been criticised for their policy not to accept cash at the turnstiles, though in fact most games do not allow purchase by card at the turnstile either and tickets can be bought by cash or card at participating supermarkets. While Swedish company Applus+ who operate the National Car Test (NCT) were forced into a u-turn on their plans to make their test centres cashless.

“Lies, damned lies and statistics” – Benjamin Disraeli (maybe*)

The European Central Bank conducted their second Study on payment attitudes of consumers in the euro area (SPACE) in 2022. Just under 2000 Irish consumers were surveyed on their payment attitudes. 54% reported cash as their main payment method by transaction count at Point of Sale (POS) with card being used by 37% and mobile apps at 6%. The use of cash in Ireland was lower than the euro area average of 59% and was a 14% drop on the 2019 figure. When it comes to value, card transactions were most popular in Ireland at 42% compared to 39% cash and considering most mobile payments are funded by a card the 6% of value by mobile app could be added to the card value.

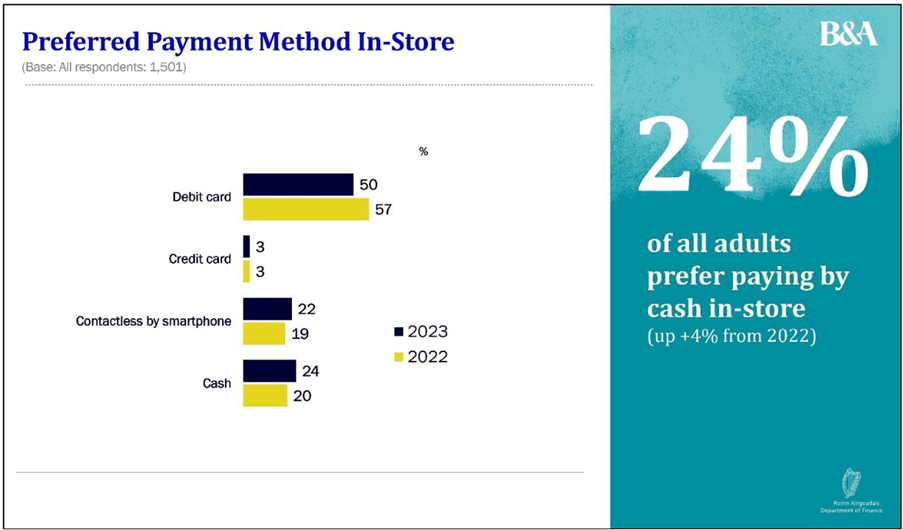

However, this survey does not seem to align with some other available data. The Department of Finance published their Consumer Banking Sentiment Survey in September 2023 and this found that cash was the preferred payment method of only 24% of respondents, albeit an increase since 2022, with debit card the preference of 50%, credit card 3% of respondents and mobile payment increasing in preference to 22%.

However, this survey does not seem to align with some other available data. The Department of Finance published their Consumer Banking Sentiment Survey in September 2023 and this found that cash was the preferred payment method of only 24% of respondents, albeit an increase since 2022, with debit card the preference of 50%, credit card 3% of respondents and mobile payment increasing in preference to 22%.

Source Department of Finance Consumer Banking Sentiment Survey 2023

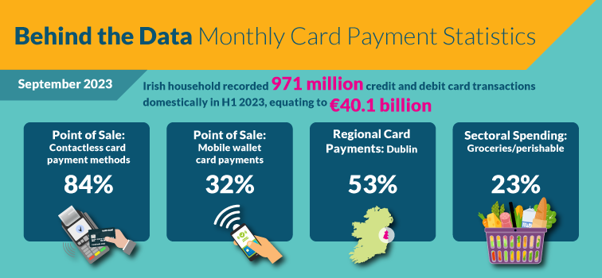

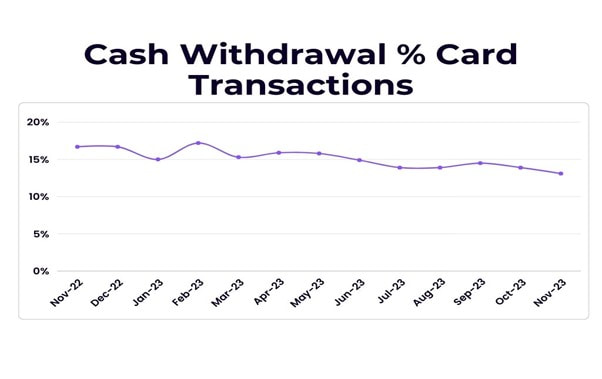

Authors graphic – source data Central Bank of Ireland Monthly Card Payment Statistics

One of the main sources of cash in the economy will be withdrawals from ATMs using debit cards. Using the Central Bank of Ireland’s Monthly Card Payment Statistics the % of card transactions by value for ATM withdrawals dropped from 18% of value in October 2022 to 13.1% of value in November 2023. The value of ATM withdrawals at just under €1.1b for domestic withdrawals has remained relatively constant but the overall value of card transactions increased by just under 37% in the same period. The stats on ATM withdrawals also include cashback at POS.

The NCT which was one of the services criticised over a planned cashless policy revealed that only 3% of transactions were made in cash.

And while not scientific I conducted my only little survey of some retailers in the first week of January to assess what they are seeing on the ground.

The NCT which was one of the services criticised over a planned cashless policy revealed that only 3% of transactions were made in cash.

And while not scientific I conducted my only little survey of some retailers in the first week of January to assess what they are seeing on the ground.

- My ‘local’ – a Dublin suburban pub: Approximately 80:20 cards to cash although they have seen an increase in cash payments in the last year.

- An Irish fashion brand with a store just off Grafton St: Majority of transactions are digital/card, when I part paid in cash at around 2pm in the afternoon I was the first cash customer they had served that day.

- An Irish sporting goods chain: The vast majority of transactions are by card, they see the odd customer paying cash.

- A café specialising in fish and chips in my hometown in Donegal: The majority of transactions are by card, last summer it was nearly all card but in the last two months they have started to see more cash transactions.

Jonathan O’Connor from New Payment Innovation Limited estimates that on average 70% of transactions are processed by card and in many city centre businesses this can be as high as 95% with increased usage of cards in hospitality compared to retail.

The fact that cash usage is slightly creeping up in some situations mirrors the case in the UK with the British Retail Consortium publishing their BRC Payments Survey 2023 in December which disclosed that cash usage in transactions increased to 19% from 15% in 2021, the first increase in cash usage in a decade as the cost of living saw it used more as a budgeting tool.

The fact that cash usage is slightly creeping up in some situations mirrors the case in the UK with the British Retail Consortium publishing their BRC Payments Survey 2023 in December which disclosed that cash usage in transactions increased to 19% from 15% in 2021, the first increase in cash usage in a decade as the cost of living saw it used more as a budgeting tool.

Choice

In the debate on cash acceptance often consumer choice is frequently referred to. However, in any purchase of a good or service there is also a seller as well as the buyer and it’s important that private businesses have the choice to set their acceptance strategies as they do today.

|   |

Authors pictures around Dublin

On the streets of Dublin, as with most other towns and cities, businesses are making a choice on whether they wish to be a cashless business, or as in the case of some of these pictures, cash only businesses.

A Cork restaurant estimated the overall cost of cash handling to their business at 9% and after trading card only would not go back to accepting cash. They succinctly put it that they “are not the only show in town” so if a customer wanted to spend cash they could choose a different business.

While some businesses have gone cashless others have ditched the card machine or are encouraging their customers to pay by cash due to rising fees. Rising fees, particularly on business to business transactions such as in the building materials sector was raised by one company last year whose acquiring fees doubled.

It will be interesting to see how the National Payments Strategy balances the question of choice when it considers cash acceptance in the future.

A Cork restaurant estimated the overall cost of cash handling to their business at 9% and after trading card only would not go back to accepting cash. They succinctly put it that they “are not the only show in town” so if a customer wanted to spend cash they could choose a different business.

While some businesses have gone cashless others have ditched the card machine or are encouraging their customers to pay by cash due to rising fees. Rising fees, particularly on business to business transactions such as in the building materials sector was raised by one company last year whose acquiring fees doubled.

It will be interesting to see how the National Payments Strategy balances the question of choice when it considers cash acceptance in the future.

What’s New

Cashless transactions are not a new function as this picture of a parking meter in Dublin City centre attests. The Card Payments Only sticker includes the Laser logo which was withdrawn 10 years ago so certain transactions have been card only for some time.

|  |

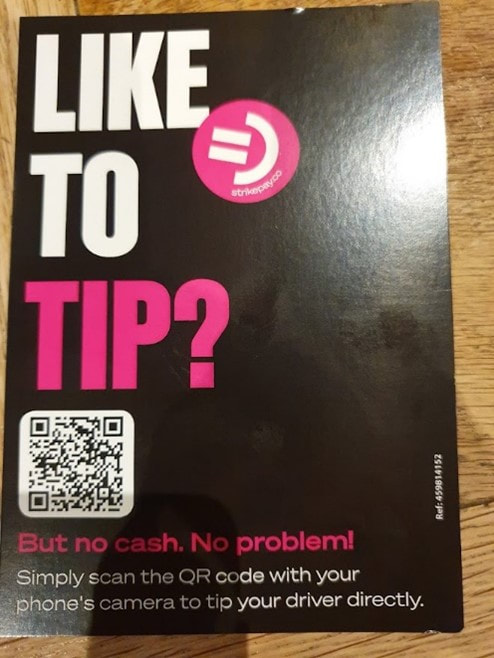

One of the areas where cash use has been prevalent is in the area of tips and it’s great to see two Irish Fintechs present solutions for this. JUSTTIP and Strikepay are supporting businesses adhere to the recent legislation on tipping using separate terminals or QR code options. Supporting my local GAA club at a fundraising bag pack in a local supermarket before Christmas, for those who wished to donate but didn’t have cash to drop in the traditional bucket they, could donate by scanning a QR code.

The one area where cash cannot be used directly of course is eCommerce. Proving that what is old, is new again, Kas$sh launched in the UK in October 2023 allowing customers to pay for online purchases using a barcode at Paypoint locations. Those involved in eCommerce for a number of years may remember similar schemes such as Ukash which was acquired by Skrill and merged with Paysafecard. While in Ireland the 3V disposable VISA cards were popular for a time and 3V was purchased by Safecharge who in turn were purchased by Nuvei.

The one area where cash cannot be used directly of course is eCommerce. Proving that what is old, is new again, Kas$sh launched in the UK in October 2023 allowing customers to pay for online purchases using a barcode at Paypoint locations. Those involved in eCommerce for a number of years may remember similar schemes such as Ukash which was acquired by Skrill and merged with Paysafecard. While in Ireland the 3V disposable VISA cards were popular for a time and 3V was purchased by Safecharge who in turn were purchased by Nuvei.

It doesn’t happen too often but if an acquirer, issuer or in this case from 2018, a scheme goes down having the fallback of cash is a good security net.

With governments looking to maintain support for cash usage, indeed the government are pumping millions of cash into the economy each week through social welfare payments paid in cash through post offices, it is likely that cash will remain in use for some time. Even Sweden, one of the countries that was envisaged as being one of the first cashless countries, has enacted legislation that the six largest banks are obliged to provide certain cash services.

The Minister for Finance has also published the Access to Cash Bill 2024 that envisages ATM infrastructure being maintained at the level of December 2022. The BPFI have called for flexibility in the scheme that would allow for demand levels to be reviewed as cash usage declines.

One of the financial institutions who are planning to invest in their access to cash are Bank of Ireland who announced a refresh of their ATM estate as part of a €60m investment in branch and ATM refreshes. However this does follow a major system issue last August that saw Gardaí being deployed at some ATMs around the country when BOI customers were able to transfer money they did not have in their account to other banks and withdraw from ATMs.

So, watch this space for the outcome of the National Payments Strategy consultation and the future place for cash.

*Mark Twain attributed it to former British Prime Minister Benjamin Disraeli but there is no proof Disraeli used this quote.

With governments looking to maintain support for cash usage, indeed the government are pumping millions of cash into the economy each week through social welfare payments paid in cash through post offices, it is likely that cash will remain in use for some time. Even Sweden, one of the countries that was envisaged as being one of the first cashless countries, has enacted legislation that the six largest banks are obliged to provide certain cash services.

The Minister for Finance has also published the Access to Cash Bill 2024 that envisages ATM infrastructure being maintained at the level of December 2022. The BPFI have called for flexibility in the scheme that would allow for demand levels to be reviewed as cash usage declines.

One of the financial institutions who are planning to invest in their access to cash are Bank of Ireland who announced a refresh of their ATM estate as part of a €60m investment in branch and ATM refreshes. However this does follow a major system issue last August that saw Gardaí being deployed at some ATMs around the country when BOI customers were able to transfer money they did not have in their account to other banks and withdraw from ATMs.

So, watch this space for the outcome of the National Payments Strategy consultation and the future place for cash.

*Mark Twain attributed it to former British Prime Minister Benjamin Disraeli but there is no proof Disraeli used this quote.

Editor (Peter Oakes): Interesting and timely piece in the UK, with the Financial Times reporting at the end of February 2024 that "Bank of England says cash still ‘hugely relevant’". The BoE said "The value and number of banknotes in circulation has increased sharply since 2020 ... Counter to the view that cash is in terminal decline, the total value of notes in circulation has risen by nearly 16 per cent, while the total volume is up by nearly 17 per cent, according to the bank’s data."

If you are interested in writing a guest article for Fintech Ireland and have us promote the fintech article to our network, get in touch along with your idea for the bones of a first draft.

| Author: Rónán Gallagher Rónán has over 20 years electronic payments experience and was a co-founder of Alpha Fintech who were acquired by PPRO in 2022. Rónán, who recently joined Fiserv at their EMEA HQ as Product Director, has worked on payments around the globe including the US, Mexico, UK, Germany, Thailand, Australia and New Zealand supporting clients including Amazon, Amadeus, Google and Meta. During one of the first Covid lockdowns with too much time on his hands he enrolled on a Masters in Innovation in Fintech with Atlantic Technological University graduating in 2022. Weekends are spent touring the pitches of Dublin, coaching GAA with CLG Chluain Tarbh/Clontarf GAA Club or cheering on his sons soccer matches. He can be reached on LinkedIn and occasionally on X on @payeire. Rónán is a Member of the Fintech Ireland Advisory Council. |